|

TSOP NO: |

3.01 |

|

SUBJECT: |

Federal Income Tax Withholding Calculation |

|

SOURCE: |

University Tax Services – Financial Management Services |

|

ORIGINAL DATE OF ISSUE: |

1/1/16 |

|

DATE OF LAST REVISION: |

2/25/16 |

|

RATIONALE: |

To provide employees at Indiana University a guide to calculate Federal taxes withheld on paychecks based on the annualized method used at Indiana University for tax withholding. |

|

PROCEDURES: |

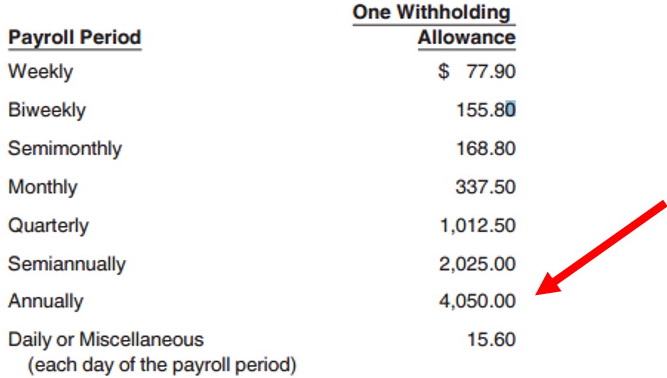

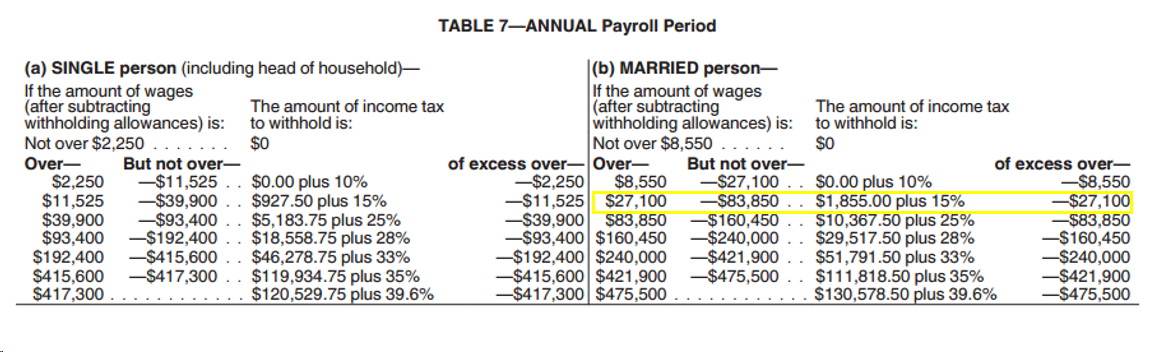

The IRS allows for different types of withholding methods to be used by employers. Prior to 2003, Indiana University used the withholding table based on whether the employee was paid on a biweekly basis or a monthly basis. Starting in 2003, we have switched withholding methods to the annualized method. The most substantial changes are occurring for those individuals that are paid on contract pay. Due to this new method, the result is little or no income tax being withheld. You may ask for additional income tax to be withheld on the W-4 and WH-4 forms. For assistance in completing the Federal form W-4, visit the IRS Withholding Calculator or the IRS Publication 919 . Annual income tax withholding method: Figure the income tax to withhold on annual wages under the Percentage Method for an annual payroll period. Then prorate the tax back to the payroll period. Example: A married person claims three withholding allowances. She is paid $3,500 a month. Multiply the monthly wages by 12 months to figure the annual wage of $42,000. Subtract $12,150 (the value of three withholding allowances multiplied by the 2016 annual allowance of $4,050 from Table 1 below) for a balance of $ 29,850 . Using the married side of Table 7 - Annual payroll period, $2,267.50 is withheld ($ 29,850 - $27,100 times 15% = $412.50, plus base $1,855). Divide the annual tax by 12. The monthly tax to withhold is $188.95. For someone that is on a 5 month contract (semester), take the monthly wage times the number of days in the contract divided by 365 times 12 to figure the annualized wage. See How is Federal Tax Withholding Calculated for Adjunct Faculty or Student Academics?

|

|

DEFINITIONS: |

Percentage Method – method prescribed by the IRS based on tables provided by the IRS for withholding calculation purposes for Federal taxes Annualized pay - How much the payee would receive if the payment was for an entire year Number of periods - The number of months, and fractions of a month, in a contract Monthly pay amount - The amount a payee will receive each monthly paycheck during the contract period Withholding allowance amount/allowance - An amount equal to one personal exemption for the current tax year Taxable income - Total income, less total withholding allowances and before tax deductions (if any) Tax rate table - A table published annually by the IRS to assist with determining tax liabilities or withholding Annual tax amount - The total amount of tax that would be withheld if the payee received the payment for an entire year |

|

CROSS REFERENCES: |

See TSOP 3.2 for Contract Pay Tax Withholding for withholding tax calculation for employees paid on contract pay (10 month pay) |