|

TSOP NO: |

8.05 |

|

SUBJECT: |

Paying Sales Tax for Purchases on Behalf of IU |

|

SOURCE: |

University Tax Services - Office of the University Controller |

|

ORIGINAL DATE OF ISSUE: |

08/02/2019 |

|

DATE OF LAST REVISION: |

05/20/2022 |

|

RATIONALE: |

To provide Indiana University Departments with instructions on when/how to utilize IU's Sales Tax Exemption while making purchases on behalf of IU. |

|

PROCEDURES: |

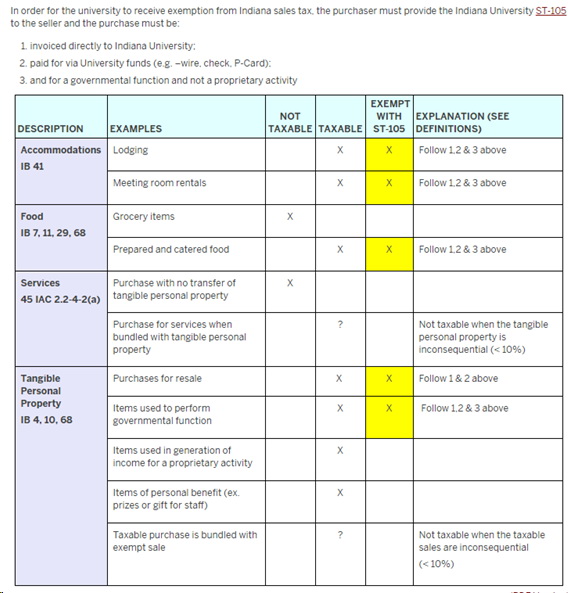

1. Examples of transactions that are exempt from sales and use tax per Indiana state law are:

2. As a state university, Indiana University is entitled to exemption from paying sales tax for sales transactions that support the following missions of the university :

3. Purchases of tangible personal property that are not related to the missions of Indiana University or that are associated with a proprietary activity are subject to tax. 4. Four factors should be considered to determine the tax treatment of a purchase:

5. The purchasing matrix below takes into account these factors to determine the tax treatment for typical purchase on behalf of Indiana University.

6. If the seller will not honor IU's ST-105 exemption certificate, that is their prerogative. Ideally, if practical, take our business elsewhere to a seller that will accept it. If that is not practical, go ahead and pay the tax, and send an email to taxpayer@iu.edu . Based on the situation and tax amount, Tax will determine whether to attempt to recover the tax from the state. 7. States do not recognize each other's sales tax exemption, but IU does have exempt status in select other states. For states other than Indiana, please visit the following webpage to determine whether IU has an exemption certificate. You will find links to those certificates, which contain instructions on what they apply to and how to use them: Sales Tax Certificates [Other States] Examples:

|

|

DEFINITIONS: |

Tangible Personal Property - means personal property that: 1) can be seen, weighed, felt or touched: or 2) is any other manner perceptible to the senses. Proprietary Activities - is defined by the state of Indiana as an activity that generates revenues for state colleges or universities from the general public and that is both customarily associated with the conduct of a private business enterprise and that is outside the scope of activities of governmental and educational functions as defined for state college or universities. Related to IU Mission - means relating to all or one of the following activities: teaching, research or public services of the university. Indiana University Student - an individual enrolled or registered in courses that grant credit toward the attainment of an undergraduate degree or graduate degree at Indiana University. K-12 Student - Includes enrolled K-12 students attending IU operated educational conferences, camp, institutes, etc. Student Organizations - are informal student clubs whose memberships consist of students who share a common interest in the particular cause or activity for which the organization exists, promotes or furthers. Educational Related Program : Class or program provided by IU, not necessarily for college credit. Does not include events held at IU by third parties or as non-educational activities. Conference Attendees : - Conference, camp or institute attendees other than IU and K-12 students. Exempt Entities : - Non-profit or governmental entities that provide appropriate proof of exempt status. (A completed ST-105 from the entity or a US Department of State Exemption card for that individual). Non-Exempt Entities : - Entities other than Tax Exempt Entities, including corporations, partnerships, LLCs, etc. Private Individuals : - Individuals (including IU employees) or their personal service corporations that sponsor conferences, camps, etc. Student Functions - An IU conducted function or activity where IU student participate. IU Department - Any department with an account in FIS NOTE: If the department bills a third party for the provided services, sales tax needs to be charged once and passed on to the third party. |

|

CROSS REFERENCES: |