Prerequisites

Prior to reading the instructions on the Account Negative Balances Report, it is beneficial to review the following sections of the IU Accounting Standards Book to gain foundational information along with report requirements and best practices:

- Accounting Fundamentals Standards Pressbook

- Chart of Accounts and General Ledger Standards Pressbook

- Financial Statements Pressbook

Overview

The Account Negative Balance Report was introduced to help locate and investigate negative asset & liability and revenue & expense balances within financial statements. Negative balance is an important process because it helps fiscal officers and users of the financial statement pinpoint and isolate issues on the balance sheet and income statement. Without reviewing for negative balances, both the income statement and the balance sheet may include balances that misrepresent the overall financial position of the entity. Reviewing for negative balances also assists entities to identify potential issues such as negative cash flows, non-collection on receivables, etc. Negative balance(s) need to be investigated and adjusted to ensure assets and liabilities are properly and accurately reported on the balance sheet according to Generally Accepted Accounting Principles (GAAP).

An asset and expense are expected to be debit balances and a liability and revenue are expected to be credit balances within financial statements unless it is an allowance code. Typically an allowance object code has a credit balance that offsets a corresponding asset or liability account. For example, an allowance for doubtful accounts acts to reduce the receivable balance for outstanding amounts that IU expects not to collect during the fiscal year. This balance is typically shown at net (the combination of both balances) within the University’s financial statements. See Accounting for Revenue Section – Write-offs and Collections for further details.

How does the Report Determine a Negative Balance

The Account Negative Balance Report is dependent on one condition:

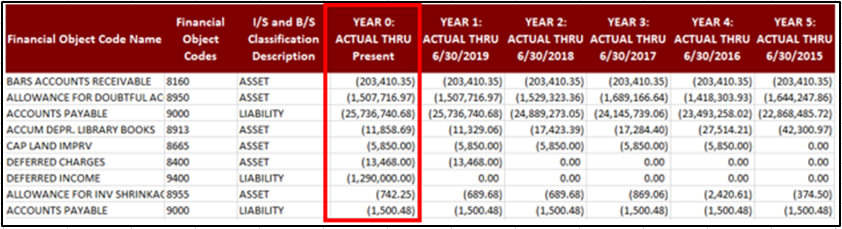

- The present balance (Year 0: Actual Thru Present) must be negative for either an asset, liability, revenue or expense as highlighted in the screenshot below.

Once this condition is met, the report generates a row showing the details related to the transaction. The report can display negative balance information going back 3, 5 or 10 years. By selecting 5 or 10 years of information, you can quickly pin-point the origin of the balances. The more often these balances are checked and corrected, the shorter the duration that needs to be selected.

The Account Negative Balance Report can be located at the top of this page - refer to the top right blue button labeled "Go to Report" which will automatically redirect users to the report within the Controller's Toolkit.

In addition, the report can be found in One.IU. To find the report, search for “Controller’s Office Reporting Tools” in the search bar, and select Controller’s Office Reporting Tools (Report Center) in the drop down menu. Mark this task as a favorite by clicking the heart icon near the start button and then select Start or click on the title.

Once in the Controller’s Tools, users will see all available reporting tiles. Navigate to the Audit Reports folder. A new tile opens which displays all of the available audit reports. Select the Account Negative Balances Report.

Running the Report

Define the search parameters to return results relevant to your organization or to a specific account. The search parameters available in the Account Negative Balance Report are divided into three parameter types: chart of account report parameters, report specific parameters and display parameters.

If there are questions related to running the report, requirements or reviewing results, please contact your (RC) fiscal officer or campus office. Each campus may have individual specific requirements related to the Account Negative Balance Report, so be sure to reach out to the related campus office or fiscal officer prior to quarter closings.

General Notes: Do not include any special characters other than approved wildcards in any of the below parameters. Additionally, do not run reports by campus as it will take up valuable computing services.

Click on a search parameter to review its definition in the Glossary.

| Parameter | Description |

|---|---|

| University Fiscal Period Code | Used to limit report to a specific fiscal period(s). |

| Chart Code | Used to limit report to one or more specific chart of accounts. For assistance determining your chart code, refer to KFS Chart Lookup. |

| Responsibility Center Code | Used to limit to a specific RC. Users are encouraged to use this parameter in conjunction with a chart of accounts code. For assistance determining your RC code, refer to KFS RC Lookup. |

| Organization Code | Used to limit report to a specific organization code. Users are encouraged to use this parameter in conjunction with a chart code. |

| Account Number | Used to limit report to one or more specific account(s). |

| Sub-Account Number | Used to limit report to one or more specific sub-account(s). |

| Object Level Code | Optional parameter to limit report to specific financial object level code(s). |

| Object Code | Optional parameter to limit report to specific financial object code(s). |

| Sub-Object Code | Optional parameter to limit report to specific financial sub-object code(s). |

| Fund Group | Limits report to specific fund group(s). |

| Sub-Fund Group Code | Limits report to specific sub-fund group(s). |

Report specific parameters are parameters specific to the generation of the report.

| Parameter | Description |

|---|---|

| I/S and B/S Classification | Used to limit report to a specific B/S classification; three options – ALL, Revenue & Expense, or Assets & Liabilities |

| Hide Fund Group | Check/Uncheck - If the user checks the Hide Fund Group, the fund group will not be displayed in the report output. |

| Hide Sub-Fund Group | Check/Uncheck - If the user checks the Hide Sub-Fund Group, the sub-fund group will not be displayed in the report output. |

| Hide I/S and B/S Classification Description | Check/Uncheck - If the user checks the Hide I/S & B/S Classification Description, the specific classifications will not be displayed in the report output. |

Display parameters are parameters that define and restrict the visual presentation of the stale balance report. They are found on the lower part of the parameters.

| Parameter | Description |

|---|---|

| Report Style | The report style parameter is used to limit level of detail required in the reports: • Consolidated – presents financial information in a consolidated format for the display level requested i.e. organization or account. • Detailed – higher level of detail showing the different accounts separately. |

| Number of Years to Display | Used to limit report to specific period; three options:

|

| Select the Output Format | Check/Uncheck - Selects whether the report is generated in Excel or HTML format. If a user selects HTML format, the report will appear in a separate tab within the user’s browser and will look identical to the excel version. Output format is based on personal preference. |

| Select the Output Destination | Once the report has finished generating in the background, a pop-up box will appear on the screen allowing you to access it. If the report takes too long to generate, the system will automatically send it to your email. |

Click Save Parameter Settings to save your parameters for future use of this report. For instructions on how to save settings, review the Save Parameter Settings document on the Controller's Office Reporting Tools page.