Prerequisites

Prior to reading the standard on Chart of Accounts – Fund and Sub-Fund Groups, it is beneficial to review the below sections to gain foundational information:

- Accounting Fundamentals Section

- Chart of Accounts - Framework Section

- Chart of Accounts - Consolidation, Object Levels and Object Codes Section

Preface

This standard discusses the chart of accounts fund and sub-fund groups and how they affect financial accounting and reporting internally at Indiana University. The information presented below will walk through a general understanding of the fund and sub-fund groups and the available groups within IU. The intent of this document is to provide a high-level overview of the fund and sub-fund groups. The functionality and appropriate usage of fund groups will be discussed in other sections of the IU Accounting Standards Book.

Introduction

Indiana University receives funds from a variety of sources, some of which restrict the general usage. Main sources of revenue to the university include state appropriations, tuition, contract and grants, and gifts. As many of these revenue sources impose restrictions on the use of the money, IU uses fund and sub-fund attributes within the chart of accounts to properly record the revenue. Fund accounting is an important concept for all public universities and is employed to ensure correct tracking of resources whose use is limited by donors, granting agencies, law, other outside individuals or entities, or by governing boards. As noted by the National Association of College and University Business Officers (NACUBO), a fund is maintained for each specific purpose. In general, fund groups categorize the characteristics and limitations placed on the resources recorded in accounts.

A fund group is used to define the broadest category of funds and is relied on for internal and external reporting. While the fund group is the broadest category of funds, the sub-fund group provides additional detail to narrow down definition and usage. On IU’s financial report, fund group attributes are divided between three categories: net investment in capital assets, unrestricted, and restricted (either internally or externally). These concepts are discussed below in detail. For unrestricted funds, the governing board (management) of Indiana University, granting organizations or government agencies can designate resources to be used for certain purposes such as student loans or capital construction (designated funds). This imposes a special stewardship obligation. IU must demonstrate that all resources are recorded and used in accordance with the directives of the outside funding sources. This stewardship obligation requires an accounting system that provides for the unique identification and recording of individual resources so that they are not commingled with other funds. By defining fund and sub-fund groups, the university is able to appropriately track and ensure money received is being spent based on restrictions.

Importance and Impact of Fund Groups

IU is a large and evolving organization with many accounting complexities, which is why the chart of accounts is critical to accurate and transparent reporting. These attributes ensure proper use of funds, compliance with applicable reporting standards, adherence to allocated budgets, and stewardship of IU resources. Categorizing financial data also allows users to understand the nature of the activity at a glance.

Use of fund groups to correctly record an entity’s finances into appropriate funds enables the university to keep revenue it receives in the proper categories and prevent revenue from being spent on inappropriate expenses. The use of fund groups within the chart of accounts also helps in the decision making process for management to ensure the best use of resources. Without the ability to ensure dollars are recorded in the correct fund type, management would be unable to accurately determine what resources are available for use for both unrestricted and restricted purposes. This can lead to a misuse of funds and compliance issues.

The fund group attributes are key in external financial and tax reporting. Not submitting or incorrectly representing the financial data for the university can have major impacts on funding and can result in fines, IRS findings and additional audit procedures. Additionally, improper use of the attributes could impact the annual external financial audit, which again, is relied upon by external users and is the official financial record and position of the university. For example, expenditures on contracts and grant funds must be in compliance with external agencies and Uniform Guidance. Fund groups are also critical for tracking on contracts and grants. Without proper allocation of money within fund groups, users can not track spending or ensure money is used in accordance with internal or external restrictions. Improper use of fund group attributes would result in IU’s inability to determine what is reportable on the required tax forms which are submitted to local, state and federal organizations.

Indiana University's Fund Types

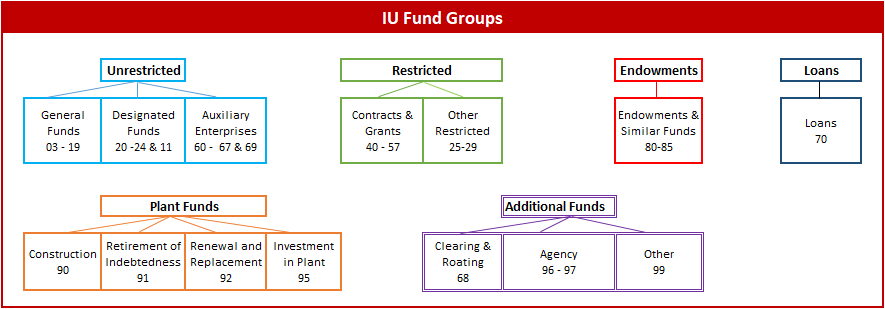

Fund types are used to classify resources into funds according to specified activities, designations, or restrictions for financial accounting and reporting purposes. These distinctions may be imposed by sponsors, donors, external regulations, or directives issued by the Board of Trustees. A fund is an accounting entity with a self-balancing set of accounts consisting of assets, liabilities, and fund balances. A sub-fund group is a further classification of fund groups to easily identify the allocation of money. The diagram to the right breaks out the hierarchy of funds.

Fund types are used to classify resources into funds according to specified activities, designations, or restrictions for financial accounting and reporting purposes. These distinctions may be imposed by sponsors, donors, external regulations, or directives issued by the Board of Trustees. A fund is an accounting entity with a self-balancing set of accounts consisting of assets, liabilities, and fund balances. A sub-fund group is a further classification of fund groups to easily identify the allocation of money. The diagram to the right breaks out the hierarchy of funds.

Fund Groups

In higher education accounting, funds are classified into one of 6 groups defined by the National Association of College and University Business Officers (NACUBO) as:

- Current funds - consists of funds expendable for operating purposes, and is divided into two fund subgroups: current funds-unrestricted and current funds-restricted. Current funds-unrestricted are available for any operating purpose of the institution and may be transferred to other fund groups such as plant funds, loan funds, or endowment funds.

- Endowment and similar funds - composed of three subgroups: (1) endowment funds, (2) term endowment funds, and (3) board-designated or quasi-endowment funds. The fund balances of donor-restricted permanent endowment and term endowment funds include donations for endowment purposes, earnings required to be added to the endowment, and net appreciation on investments that is subject to future appropriation for spending. At Indiana University, term endowment sub-fund group is generally not utilized.

- Loan funds – categorized as restricted or unrestricted, but grouped in the same fund. Restricted loan fund balances include donor and governmental funds restricted for purposes of making loans, endowment earnings specified for loans, and interest income on loans previously issued from restricted loan funds. Unrestricted loan fund balances include funds designated by the board for loan purposes.

- Plant funds - consists of up to four sub-funds, as follows: (1) unexpended plant funds, (2) funds for renewals and replacements, (3) funds for the retirement of indebtedness, and (4) investment in plant. Plant fund balances may include funds contributed by donors for plant construction or acquisition, student fees raised for construction or for the payment of interest and principal on debt, amounts held in reserve in the funds for the retirement of indebtedness or funds for renewals and replacements in accordance with externally imposed bond indentures.

- Annuity and Life Income Funds - used to account for assets provided by donors under split-interest agreements and the obligations to make payments to the beneficiaries of those agreements. The agreements specify how the benefits of the assets of the fund are shared between the institution and the beneficiary(ies). Currently at IU, this fund group is used exclusively for the Riley Hospital Endowment.

- Agency Funds - resources held by an institution as a custodian or fiscal agent for others, such as student organizations, individual students, faculty organizations, or individual faculty members. Agency funds have only assets and liabilities and do not include individual revenue or expense transactions of the institution.

At Indiana University, fund types are used to classify funds with similar funding sources that are consolidated into one of the below fund groups. Separate funds are maintained within each fund type to insure compliance with limitations and restrictions placed on the use of resources. Within Indiana University, we have 14 fund groups and more than 50 sub-fund groups. See here for a full list of the available fund and sub-fund groups. Users are not able to create a new fund group document, but users can select both the appropriate fund and sub-fund groups. The fund groups are broken up into the below categories.

Unrestricted Funds

Include those economic resources of the institution which are expendable for any purpose in performing the primary objectives of the institution, i.e. instruction, research, and public service and which have been designated by the governing board for a specific purposes.

Unrestricted funds do not have rules for use placed by the source of the funds. Only university business rules are applicable for use of unrestricted funds. Examples of sources of unrestricted funds would be tuition and fees and funds from sales and services. The unrestricted fund groups at IU are discussed below. Note - for full list of available sub-funds by campus and account prefix, see quick reference document.

Click on the link below for full definition of fund group.

| Fund Group Name | Major Sub-Fund Group | Account Prefix Number |

|---|---|---|

| General Fund | N/A | 03-19 |

| Designated Fund | Continuing Education, Public Services, Internal Research, Other | 20, 21,22, 23 |

| Auxiliary Enterprise Funds | Auxiliary Funds , Service Funds | 60-67 & 69 |

Restricted Funds

These funds have specific requirements and/or intentions for use set by the funding source. Examples would be funds from a donor or funds from a specific research contract or grant. Restricted sub-funds at IU include:

| Fund Group Name | Major Sub-Fund Group | Account Prefix Number |

|---|---|---|

| Contract & Grant Funds | N/A | 40-57 |

| Other Restricted Funds | Fellowships, Scholarships, Special State Appropriations, Matching Endowments and Restricted Other | 25, 26, 27, 28, 29 |

Loan Funds

| Fund Group Name | Major Sub-Fund Group | Account Prefix Number |

|---|---|---|

| Loan Funds | Internal Loan Fund and Loan Funds | 70 |

Endowment and Similar Funds

Endowment funds are primarily used for scholarships and some faculty support; received from interest paid on invested donor gifts. In general the IU Foundation is the main recipient of endowments and IU does not typically receive endowments unless IU is specified by the endowment (i.e. IU is named as the beneficiary).

| Fund Group Name | Major Sub-Fund Group | Account Prefix Number |

|---|---|---|

| Endowment Funds | N/A | 80 |

| Life Estate Funds | N/A | 82 |

| Quasi Endowment Funds | N/A | 81 |

| Riley Hospital Endowment Funds | N/A | 83-85 |

Plant Funds

Plant funds are primarily used for new construction, renovation and building repairs and maintenance. These fund groups are managed centrally either through manual entry or automatic batch entry.

| Fund Group Name | Major Sub-Fund Group | Account Prefix Number |

|---|---|---|

| Construction Fund | N/A | 90 |

| Retirement of Indebtedness Fund | N/A | 91 |

| Renewal and Replacement Fund | N/A | 92 |

| Investment in Plant Fund | N/A | 95 |

Additional Funds

| Fund Group Name | Major Sub-Fund Group | Account Prefix Number |

|---|---|---|

| Clearing and Rotating Funds | N/A | 68 |

| Agency Funds | Internal Agency Fund , External Agency Fund , Work Study Agency Fund | 96, 97, 98 |

| Component Unit Agency Funds | N/A | multiple accounts |

| Other Funds | Other Fund | 99 |

Requirements and Best Practices

This section outlines requirements related to the Chart of Accounts – Fund and Sub-Fund Groups, as well as best practices. While not required, the best practices outlined below allow users to gain a better picture of the entity’s financial health and help identify potential issues on a more frequent basis. This allows organizations to identify errors, mistakes and pitfalls which can be remedied quickly and prevent larger issues in the future.

Requirements

- Fiscal officers should be knowledgeable of all the Chart of Account- Fund and Sub-Fund Groups standard listed within the document. In addition, fiscal officers should review the accounting Glossary to gain pertinent knowledge of accounting at IU.

- It is the responsibility of the fiscal officers to ensure the proper usage of individual fund and sub-fund groups during the selection process. Contact your RC fiscal officer or campus business office for internal reporting requirements related to proper fund group usage.

- If users have questions regarding the chart structure or attributes, contact the University Accounting and Reporting Services team at uars@iu.edu.

Best Practices

- For additional information on the structure of the chart of accounts, attend the KFS Training Series held by the Financial Training & Communications team. Register by visiting the training website.